2016 wrapped up for the data center Big 6 public providers (EQIX, DLR, CONE, DFT, QTS and COR) with stable to modestly improving price dynamics, and a supply/demand balance in most markets.

While pricing has been stable for the last few years, it is the industry’s continued commitment to underwriting deals based on sustaining ROIC and investor returns in the face of increasing competition that maintains price stability.

Overall, pricing and supply/demand fundamentals going into 2017 are solid as evidenced by industry metrics, and a general consensus of service provider market sentiment. These market dynamics are additionally supported by recent WiredRE data center research in various U.S. data center markets.

Following are metrics and excerpts from 2016 FYE earnings calls and presentations from the Big 6 public data center providers. The data for the most part supports stability in both price and supply/demand balance dynamics.

![]()

- …we continue to invest and expand globally, putting to work over $1.1 billion in CapEx in 2016. We have 19 announced expansion projects underway, as we respond to strong supply demand conditions across all of our operating regions.

![]()

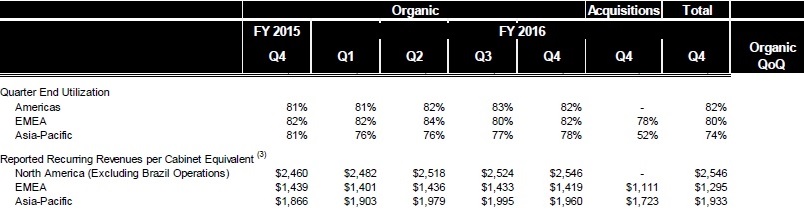

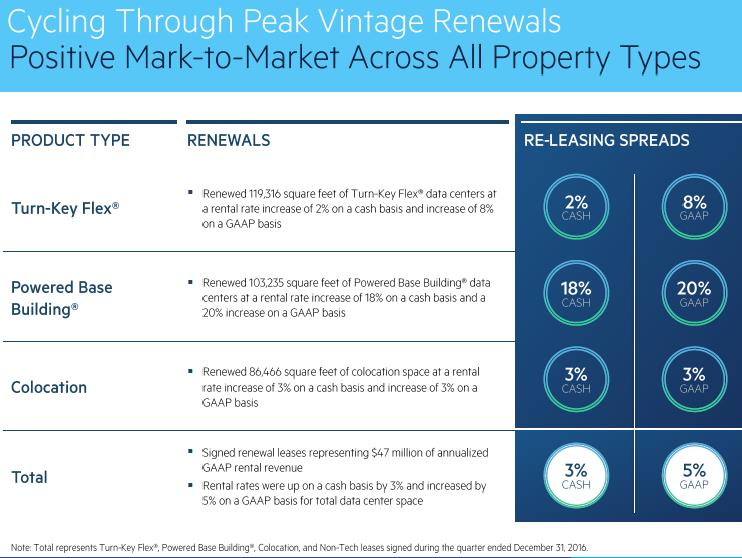

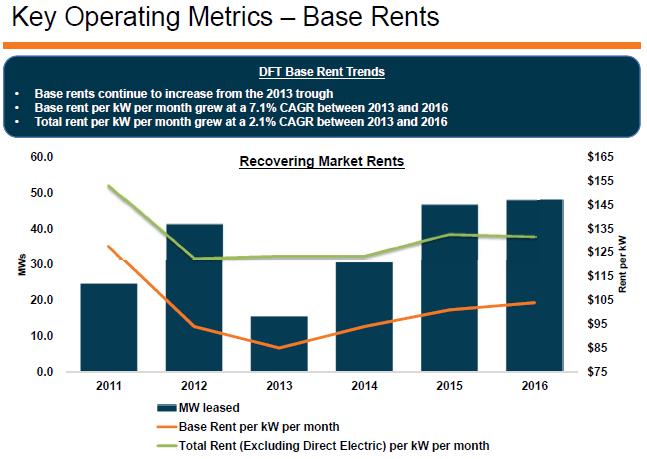

Click charts to enlarge.

![]()

- Our competitors are largely behaving rationally. But we have seen an uptick in fresh capital targeting the sector. To date, recent investments have mostly been focused on stabilized assets, perhaps reflecting a tacit acknowledgment that barriers to entry may be higher than meets the eye.

- The floodgates have opened for data center packages coming to market, but the supply of products on the market has not depressed pricing.

- New Jersey continues to be our weakest market. I wouldn’t say that there is irrational pricing there. There just is weak demand. I think where you find potentially irrational pricing is when there is a significantly sized deal, a very large deal that you’ll find people that – who price very competitively for those.

![]()

- Pricing this quarter increased 38% versus the trailing four quarter average.

![]()

- DFT experienced strong renewal pricing in 2016. Upon the expiration of the original lease terms, cash based rents will be an average 3.6% higher and GAAP based rents will immediately be an average of 3.1% higher.

- …even though we are likely to see pricing pressure, we believe that the pressure will be positively offset by two factors: first, the elimination of risk from our development pipeline as large leases with high credit names become the norm; and second, our ability to achieve targeted development yields through the design flexibility of our premium data centers.

![]()

- New and modified leases pricing up 16% compared to P4QA (prior 4 quarter average).

- C1 pricing 9% above P4QA due to mix of smaller C1 deals signed and continued positive pricing trends across our markets.

- C2/C3 pricing ~40% above P4QA due to several large C3 deals signed in Q4.

- Renewal rates up 4.7% compared to pre-renewal rates.

- Commenced leases: C1 pricing decline due to higher mix of larger C1 commencements which also drove increased volume.

- Commenced leases: C2/C3 pricing also down due to higher mix of relatively larger footprint C2 deals.

- Overall, the pricing environment across to our footprint remains strong and is consistent with the positive market trends that we’re seeing.

- Obviously it is a very competitive environment out there, but we see sort of rational behavior out there. We see supply not getting too far ahead of demand, in our markets. We think that is relatively balanced, and it doesn’t take away that every deal is very competitive…

![]()

- As it relates to our largest markets, we’re seeing steady demand and a consistent balance with supply in Los Angeles. In the Bay area, capacity across the market remains relatively lean while demand remains quite healthy, with pricing remaining firm.

- Supply and demand seemed generally in balance on the wholesale side in most of our markets. However, we are mindful of reports of increased appetite from privately funded developers.

- Our renewal pricing reflects mark-to-market growth of 2.9% on a cash basis and 5.5% on a GAAP basis. For the full year, our cash rent growth is 3.9% in line with the midpoint of our guidance.

- Regarding Northern Virginia and DC, we continue to see robust demand particularly from the enterprise vertical. Although supply appears to be increasing, the current environment remains well balanced and our leasing pipeline is healthy.

- …we have seen some positive momentum in the New York, New Jersey market with an increase in the pace of leasing in Q4. Demand continues to be concentrated among smaller customer requirements with very good traction among enterprises and more specifically the financial services industry.

Rational Behavior: A new evolving theme is the recognition that irrational pricing and supply decisions erode market stability for all participants. Bill Stein (DLR CEO) first mentioned rational peer behavior during his Q3 2016 earnings call. In Q4 2016 earnings calls Stein mentioned it again along with Chris Eldredge (DFT CEO) and Dan Bennewitz (QTS COO). The commentary is important as it refers to the maturing nature of the data industry as a whole, and the commitment amongst providers to maintain the integrity of the value of these long-term fixed assets which they deserve.

Recent Research Highlights:

2017-2020 Data Center CAPEX Investment: https://wiredre.com/40-billion-capex-spend-for-big-6-u-s-data-center-companies-2017/

Investment Bank Advisory: https://wiredre.com/wiredre-completes-international-market-advisory-for-top-5-investment-bank-2016/

Infrastructure Cost Perspectives: Cloud, Colocation, Build-To Suit: https://wiredre.com/infrastructure-cost-perspectives-cloud-colocation-build-suit/